Korea to become next fintech hub

LENDIT CEO Kim Sung-joon speaks about the potential of financial technology, or fintech, in Korea, in an interview at the company’s headquarters in central Seoul, on Oct. 21. / Courtesy of LENDIT

Centralized finance management system key driving force for fintech industry

By Lee Min-hyung

Banking and finance have long been among the most heavily regulated industries in any country, as their potential fallout causes worst-case scenarios affecting every part of all other businesses.

Financial technology, more commonly called fintech, has for this reason failed to grow fast enough to catch up with the speed of overall technological development in other industries.

Given that financial transactions are the backbone of all economic activity, the potential of fintech to expand is more promising than in any other industry, according to peer-to-peer (P2P) lending platform operator LENDIT CEO Kim Sung-joon.

“Korea is at the initial stage of embracing fintech, compared with other industry-leading marketplaces such as the United States or the United Kingdom,” the 31-year-old CEO said in an interview.

“But the fintech market here is getting more activated and popularized, as Korea is on a path to deregulate for emerging fintech business,” he said. “In the U.S. and China, the fintech market is growing fast, due to their open environment toward regulations.”

No matter how fast the government shifts its stance and deregulates the industry, it can never catch up with the speed of the industrial revolution, according to him.

But he expressed optimism for its potential for growth, citing Korea’s market size and centralized debt-management infrastructure.

“Korea has tight and centralized financial information management infrastructure, which is why I believe the nation will become one of the world’s most influential fintech powerhouses,” he said.

“There are only a limited number of countries

including the U.S., U.K., Australia, Germany and Korea

where the government pushes for a centralized policy when it comes to financial information management.”

This means the government can manage massive sets of big data coming from transactions of its population, he said. Collected big data can then be used to create enormous numbers of algorithms. The designer-turned-entrepreneur said those algorithms are the driving force of innovation.

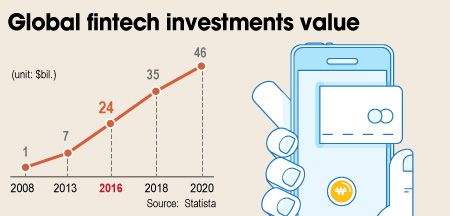

According to German-based market research institution Statista, the volume of global fintech investment is expected to surpass $46 billion in 2020, a whopping growth from some $1 billion in 2008.

Kim earned a bachelor’s degree in industrial design at Korea Advanced Institute of Science and Technology (KAIST).

He has received a number of globally renowned design awards

including Spark Awards, the International Design Excellence Awards (IDEA) and Red Dot Award: Communication Design.

He then went on to study product design at Stanford University, but dropped out to pursue his goal of running his own company.

The LENDIT CEO said he decided to establish the company in March 2015 after California-based P2P lending operator Lending Club met explosive success there.

He was confident that the U.S. online P2P model could bring a similar level of success in Korea, given the nation’s government-led, systemized debt-management system.

“Korea’s lending market is worth about one fourth that of the market in the U.S.,” he said. Considering the difference in GDP per capita, the size of Korea’s lending market is incomparably big compared to any other country, according to him.

“On top of that, Korea is a much safer lending market due to its low default rate than the default rate in the U.S.,” he said.

“We collected some 800,000 big datasets in Korea to analyze investment patterns of each investor,” he said. “The big data allowed us to create a ‘recommended algorithm’ for investors. This is then used to create a more specific and personalized investment portfolio for them to reinvest on our platform.”

LENDIT is currently the nation's top-tier P2P lending operator. The company has grown rapidly to have lent a total of more than 21 billion won in just 18 months after its foundation in March last year.

“Our short-term goal is to innovate different fintech sectors, beyond P2P lending, in five to seven years,” he said.

Partnership over rivalry against big capital

With P2P lending growing rapidly around the globe, increasing numbers of financial service giants are casting more influence on the market.

But Kim dispelled concerns over any potential rivalry against big capital, citing a win-win attitude of the financial giants in other sectors.

“Most big financial service providers put a partnership with new fintech operators over a cutthroat rivalry,” he said. “If traditional financial institutions push for an aggressive expansion strategy into new areas, their brand image will be overlapped. They shun away from this type of competition, as a strong, reliable brand identity is considered most important.”

“For instance, an automobile insurance service operator never publicly advertises their financial products in other areas

including credit loan services,” he said. “They instead seek to expand their presence in new areas by forming partnerships and investing with existing players.”

This is the same in the U.S. market, as the P2P industry has began to grow faster when big financial firms there tapped into the area by increasing their investment through partnerships, he said.