Household debt woes deepen with looming interest rate hike

gettyimagesbank

OECD cites household debt as major downside risk

By Yoon Ja-young

With the central bank signaling an earlier-than-expected key interest rate hike, the country's record-high household debt is emerging as a major downside risk to an economic recovery, prompting economists to call for a cautious approach in policymaking to ensure a soft landing.

The country's key rate has been maintained at 0.5 percent for a year, but Bank of Korea Governor Lee Ju-yeol recently hinted at a shift in monetary policy toward credit tightening in the months to come. He did not rule out the possibility of moving ahead of the U.S. Fed, which is expected to come out with a rise in the latter half of next year at the earliest.

Some foreign investment banks expect a key rate hike could come within this year based on Lee's signals, and there have already been signs in the market that interest rates are on an upward spiral.

The yield on 10-year Korean treasury bonds rose for four consecutive days to 2.202 percent June 2, surpassing the 2.2 percent mark for the first time since November 2018. According to the central bank, commercial banks were levying an average 2.91 percent interest rate on new household loans in April, up 0.03 percentage points from the previous month, and the highest level since January last year before the country was hit by the pandemic.

Record-high household debt

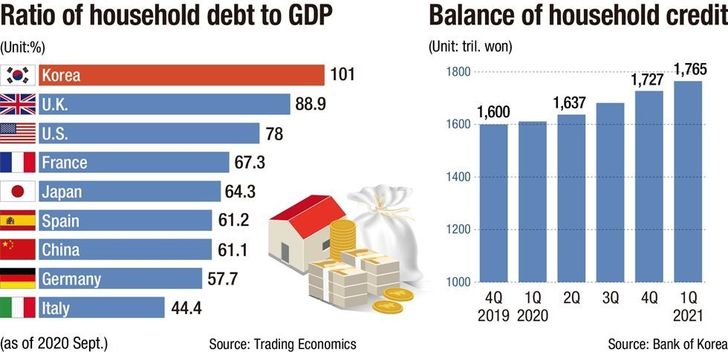

Increasing borrowing costs are adding to the burden of household debt. The country has a high ratio of household debt to gross domestic product (GDP) compared with most other major economies, a perennial risk for Korea Inc.

The ratio for Korea stood at 101 percent in September, 2021, well above the U.K.'s 88.9 percent, the U.S.'s 78 percent, Japan's 64.3 percent and China's 61.1 percent.

The Organization for Economic Cooperation and Development (OECD), which recently revised up its economic growth outlook for Korea this year by 0.5 percentage points to 3.8 percent from its March estimate based on positive factors such as strong export growth and rising investment, also picked household debt as a risk.

“Volatility in house prices and high household debt, which amounts to more than 160 percent of net household disposable income, could threaten financial and macroeconomic stability,” it noted.

The balance of household debt, including credit card payments, recorded 1,765 trillion won as of the end of the first quarter, up 154 trillion won from a year ago. It was the biggest rise ever despite the regulator's restrictions on loans. Of the total debt, 931 trillion won was mortgages.

Many households are vulnerable to rising interest rates as fixed-rate borrowings account for only 27 percent of all loans as of April. According to central bank data submitted to Rep. Yoon Doo-hyun of the main opposition People Power Party, a 1 percentage point interest rate increase will add 11.8 trillion won to what households already owe lenders.

Economists note that this could hamper economic recovery.

“As the burden in paying back loans grows on households, there is a risk of it hindering economic growth,” said Lee Boo-hyung, a director at the Hyundai Research Institute.

He pointed out that while the government let small business owners delay payment of debt as they were on the verge of closing due to COVID-19, their capability to pay back loans has only worsened.

While disposable income will decrease under pressure from the growing burden of debt, uncertainties in the job market add to the problem, according to Lee.

“The rising interest rate should be offset by an increase in household income, either through job creation or wage increases. If the job market doesn't pick up as much as the economic recovery, consumption will remain restricted due to the burden of debt,” he said.

LG Economic Research Institute economist Lee Geun-tae identified the self-employed as the most vulnerable group.

“What is concerning is that things have been harsh for the self-employed, and their debt has increased considerably. When interest rates rise, this risk could expand. “

The impact on the assets market is also noteworthy as any rate hike can move liquidity to bonds from other assets. The KOSPI has already become stagnant due to uncertainties over monetary policy, but analysts say it will differ by sector. While mortgages account for over 50 percent of household debt, housing prices aren't likely to be impacted much. Sectors that have been floating on abundant liquidity, meanwhile, will see some corrections.

“Housing supply is restricted so the prices aren't likely to see a steep correction despite an interest rate hike. Cryptocurrencies and growth stocks such as bio firms, meanwhile, are likely to experience some shock from a rate hike,” said the Hyundai Research Institute's Lee.

Analysts say a key rate hike, which is inevitable, should come in a manner that induces a soft landing. The OECD noted in its report that Korea needs a prudential policy “to contain risk-taking and the build-up of household debt.”

“To minimize the risk from growing household debt on interest rate increases there should be continued efforts to improve the quality of the household debt situation,” Lee said.