KEPCO bonds aggravate fears of corporate credit crunch

The headquarters of Korea Electric Power Corporation (KEPCO) located in Naju city, South Jeolla Province / Newsis

Heavy issuance of state-run electric power company shakes bond market

By Anna J. Park

A massive volume of bonds issued by the Korea Electric Power Corporation (KEPCO) throughout this year has been jolting local corporate bonds market, becoming a source of stress on already strained corporate bonds and commercial paper (CP) markets in the country.

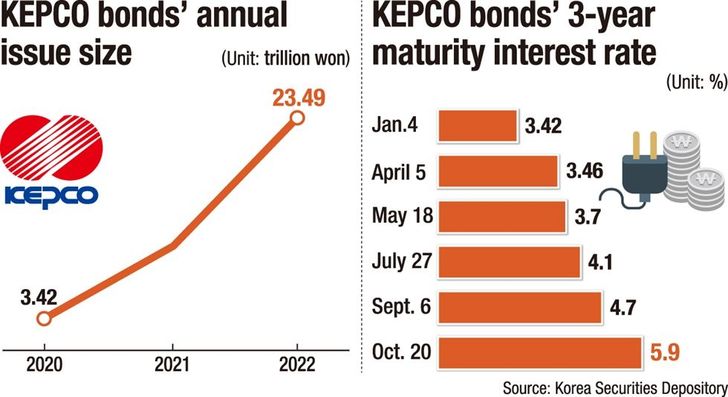

According to data by the Korea Securities Depository (KSD) Thursday, KEPCO has so far issued bonds worth 23.49 trillion won ($16.57 billion) this year. The amount is already more than double of the entire size of KEPCO bonds issued last year. On average, it means the state-run electric power company has been providing two to three trillion won worth of top-notched credit bonds every month this year; this month alone, the power company has issued over 1.73 trillion won worth of bonds.

The excess supply of top-rated KEPCO bonds every month into the local corporate bonds market, amidst globally soaring interest rates and tightening monetary policies, resulted in a further rise of corporate bond interest rates. As the three-year maturity interest rate for KEPCO bonds rose to more than 5.9 percent in late October ― the highest level in 14 years ― other corporate bonds also face a higher burden of increasing additional interest rates for their corporate bonds to attract creditors.

As a consequence, KEPCO bonds are sucking in market liquidity and demand like a giant black hole with their top-rated stable status as well as near six percent interest rates, crowding out other companies' bonds in the credit market. Now corporations that are in need of borrowing money find it harder than ever to sell their bonds.

Market experts agree that the massive supply of KEPCO bonds every month has been one of the factors aggravating current credit crunch concerns in the local corporate bonds market.

“The supply of top-rated bonds, including KEPCO bonds and bank notes, has played a part in the recent credit market deterioration, creating a crowding-out effect; bonds that are rated less than triple A credit status has been somewhat driven down from the market,” Baek Doo-san, analyst at Korea Investment & Securities, said.

“The increased issuance of special bonds like KEPCO bonds delays the recovery of corporate bonds market,” Chung Dae-ho, another credit market analyst from KB Securities, pointed out, adding that the state-run electric power company is expected to continue bond issuance until next year.

Gov't faces dilemma over KEPCO

The real problem is that the government is facing a huge dilemma in their next moves over KEPCO's massive deficit. Due to global energy price hikes, the state-run power company suffered an operational loss of 14.3 trillion won during the first half of this year, and it is expected to post an annual deficit of around 30 trillion won this year. It is nearly six times from last year's annual deficit of 5.86 trillion won. The key to solve the deficit lies in raising the country's electricity bills, but it's not an available option for the government, considering the inflation rate.

Given the mounting deficits, KEPCO might have a liquidity problem if it stops issuing bonds every month. However, concerns in the local corporate bonds market are also growing, following a defaulting of 205 billion won asset-backed commercial paper (ABCP) issued by Gangwon Province-led Legoland Korea developer earlier this month.

Even KEPCO bonds cannot find enough creditors to buy the entirety of its bonds in the local market, despite the top-rated credit status and high interest rates. The continual issuance of KEPCO bonds could contribute to making other corporations' short-term funding harder.

Some market insiders suggest selling KEPCO bonds in overseas market, rather than in local markets. Some other experts urge the government to take a more proactive approach in stabilizing the short-term funding market.

“While the government is drawing up a series of measures, such as immediate implementation of bond market stabilization funds and the delay of banks' LCR normalization, stronger measures aimed at stabilizing the market seem necessary to turn back the overall market sentiment,” Lee Kyoung-rok, analyst at Shinyoung Securities, said.

In response to such calls, the Bank of Korea (BOK) announced Thursday afternoon that it adds KEPCO bonds along with bank bonds to the BOK's list of qualified securities, aiming to reduce financial companies' liquidity burden. Currently, various government-issued bonds and Korea Housing Finance Corporation's mortgage-backed security are listed as BOK's qualified securities.

Meanwhile, the aggregate amount of bonds issued by local corporations in September stood at 16.4 trillion won, a 19.8 percent decrease from the previous month and a 6.5 percent fall year-on-year.