Finance minister opposes demands to increase supplementary budget

Finance minister Hong Nam-ki speaks during a parliamentary budget committee meeting at the National Assembly in Seoul, Monday. Yonhap

Fast-growing sovereign debt concerns fiscal soundness

By Anna J. Park

A tug-of-war continues between the National Assembly and Finance Minister Hong Nam-ki over the allocation of the supplementary budget. While ruling and opposition party lawmakers are asking for further increases of the supplementary budget, the finance minister opposes the idea on concerns of a possible downgrading of Korea's sovereign credit rating as well as the stabilization of the government bond market.

During the National Assembly's Special Committee on Budget and Account meetings held on Monday and Tuesday, Hong made clear his point that the country's repeated supplementary budget allocations due to the global pandemic situation have been risking Korea's global credit rating.

“Global credit rating agencies are concerned over both the speed of the country's debt increase rate as well as a failure to keep fiscal discipline under control at the parliament,” Hong said during the committee meeting.

The finance minister reiterated his stance that the large supplementary budget demanded by parliament would be difficult to approve.

Ahead of the presidential election, the government submitted a supplementary budget plan of 14 trillion won ($11.7 billion) to the National Assembly in January. But the supplementary budget plan could be increased to over 39 trillion won, as the National Assembly's Trade, Industry, Energy, SMEs and Startups Committee submitted a bill to increase the supplementary budget by 24.9 trillion won from its previous 14 trillion won. Given that both the ruling and opposition parties are proposing additional supplementary budget bills, the budget could reach up to 50 trillion won.

“The 14 trillion won supplementary budget by the government is unprecedented in size compared to previous additional budget plans ever made in January,” Hong stressed. “While fine tuning the plan could be possible, another supplementary budget of two to three times the size of the current addition would be difficult to approve, given its potential negative side effects,” he added.

Soaring treasury yields and the accompanying shock to the local financial market are also concerns voiced by the ministry. Responding to the potential supplementary budget plan of up to 50 trillion won, the yield on three-year treasury bonds rose to 2.303 percent on Tuesday, up 0.066 percentage point from the previous day. It was the first time in three years and nine months that the three-year treasury bond rate exceeded the 2.3 percent mark.

This year alone, the three-year treasury yield hiked by 0.505 percentage point on concerns that the government would increase the issuance of government bonds to cover the supplementary budget plan. Some market analysts forecast that the three-year treasury yield could reach over the 3 percent range, if the Bank of Korea increases its key interest rate to over two percent and the government's hefty spending continues.

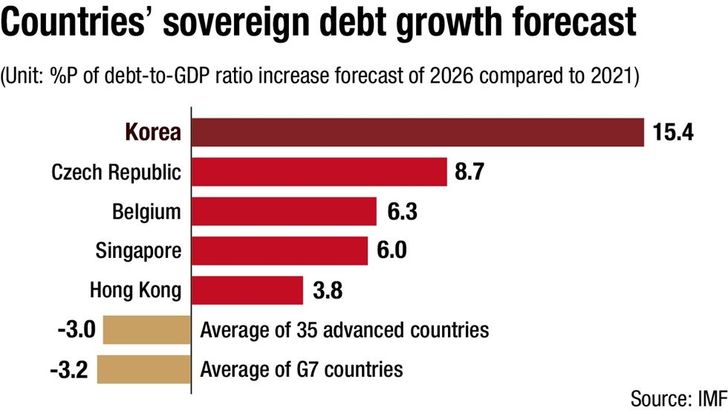

Actually, a report by the International Monetary Fund (IMF) late last year warned that Korea would mark the highest sovereign debt growth rate among 35 developed countries. The report forecasts that the Korean government's debt-to-GDP ratio would reach 66.7 percent, which is 15.4 percentage points higher than the 51.3 percent logged by the end of 2021.

As the report shows, Korea's sovereign debt has increased rapidly during the past five years. The sovereign debt is expected to reach some 1.07 quadrillion won by the end of this year, from some 660 trillion won logged in 2017.

Late last month, the IMF slashed Korea's economic growth outlook for this year to 3 percent from its previous 3.3 percent, advising the government to reduce the fiscal deficit that has increased considerably. Fitch Ratings also warned that the continual increase of the country's sovereign debt-to-GDP ratio could be a pressuring factor for lowering Korea's credit rating in the long term.