Korea's total household credit hits new high in Q2

Song Jae-chang, chief of the BOK's financial statistics team, speaks during a press conference at its headquarters in Seoul, Tuesday. Courtesy of Bank of Korea

By Lee Min-hyung

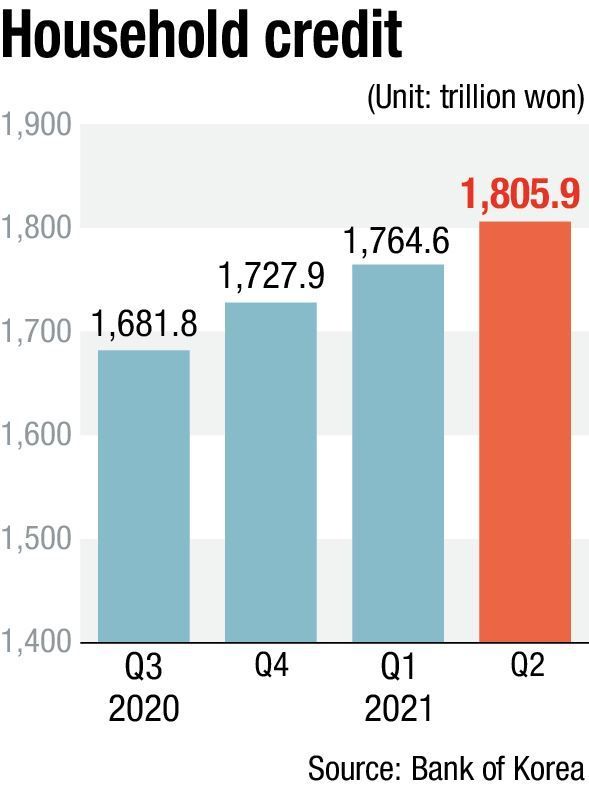

Korea's total household credit set a new high of 1,805.9 trillion won ($1.54 trillion) as of June due to an uncontrollable frenzy for leveraged investments and increases in post-pandemic living costs, the Bank of Korea (BOK) said Tuesday.

“Household credit” is a Korean term for the total amount of debt held by all households of the nation, including household debt, as well as loans taken out at conventional financial institutions and credit purchases that have not yet been paid.

The figure is a 10 percent increase, year-on-year, and the highest the central bank has noted in the 18 years it has been recording the data, according to the BOK. On a quarterly basis, total household credit rose by 41.2 trillion won, or 2.3 percent.

The increase was driven by growing demand for mortgage loans as well as increased costs of living for people struggling amidst the prolonged coronavirus pandemic, the central bank said.

“Demand for loans used for housing purchases and 'jeonse' lump-sum rental payments continued to remain steady throughout the second quarter,” Song Jae-chang, chief of the BOK's financial statistics team, told reporters during a press conference.

With households taking out more loans to buy stocks ahead of big firms' initial public offerings during the April-June period, household credit reached a new high during the period, the BOK official said. Small business owners and the self-employed also relied more on loans for living expenses amid the tight social distancing measures, according to the central bank.

Since the pandemic outbreak in early 2020, the figure has been on a rapid rise, in line with soaring housing prices here. It has also continued growing at an alarming pace due to a super-low interest rate after the BOK cut the benchmark rate to 0.5 percent in May last year.

With the excessive level of household lending emerging as a major social problem, financial authorities have been stepping up their warnings against offering loans to households, urging banks to tighten their lending practices.

The BOK is also set to increase the key rate at its upcoming monetary policy board meeting, slated for Aug. 26, with a view to stopping the already-overheated asset market from falling into a frenzy and to help slow down the rapid increase in household lending.

“We cannot say for sure that the possible rate hike will definitely curb the rising level of household debt, but the central bank expects the move to help slow down the pace of its growth,” Song said.

Even before the projected rate hike from the monetary authority, commercial banks are on track to increase their interest rates for loan products.

The nation's top four banks ― KB Kookmin, Shinhan, Hana and Woori ― raised the interest rates for their non-collateral loan products by around 1 percent to an average of around 2.96 to 4.01 percent as of Aug. 19, compared to last year. Interest rates for their mortgage loans have also been on the gradual rise during the same period.

Financial watchdogs, such as the Financial Supervisory Service (FSS) and Financial Services Commission (FSC), are considering introducing stricter loan regulations based on their fears that households may fall victim to a possible perfect storm.

The FSC has recently cut the individual credit line for non-collateral loans in half, to an amount equal to a borrower's annual salary. FSC Chairman nominee Koh Seung-beom is also threatening to mobilize all possible measures to control surging household debt.

Economists say that the watchdogs need to find a middle ground while pushing for the regulation so as to minimize any possible side effects.

“The financial authorities are moving to introduce additional regulations to curb soaring household debt, as the monetary policy is not enough to control it,” Korea University economist Kim Jin-ill said.

“As the government carries out this tougher set of regulations, some people may fall victim (to getting caught between the high cost of living amidst the pandemic-caused economic downturn and the inability to access loans),” he said. “The key lies in how to minimize the side effects by watching the atmosphere of the market closely.”

Sejong University economist Kim Dae-jong urged the government to introduce a “predictable” set of regulations before announcing new loan regulations.

“If authorities continue to carry out measures that are unpredictable, public backlash will escalate further, which will end up confusing the market.”