INTERVIEW Investors advised to find opportunity amid virus crisis

Martin Horne, Barings' Head of Global Public Fixed Income & Head of Global High Yield / Courtesy of Barings

Barings' fixed-income chief highlights high-yield bond investment

By Anna J. Park

No one can be sure how the current virus-led economic slowdown will play out in the near future, as global market volatility has widened extremely amid uncertainty.

In this murky economic outlook, however, experienced investors still find a silver-lining and make the best out of the pathogen-caused crisis.

In a recent email interview with The Korea Times, Martin Horne, global investment firm Barings' Head of Global Public Fixed Income and Global High Yield, stressed a strategic and through-the-cycle approach when it comes to choosing investments.

The financial expert, who's been in the industry since 1996, now holds primary responsibility for European High Yields, Structured Credit and Emerging Market Corporate Debt Investment Groups. Barings operates over $338 billion as of the end of last year, with some 2,000 professionals located in 16 countries.

Horne particularly emphasized that careful investment into high-yield bonds ― bonds that pay higher interest rates as they have lower credit ratings than investment-grade (IG) bonds ― could be an option for those wishing to rake in handsome returns.

It might sound counterintuitive that he recommends investors of high-yield bonds, as in laymen's eyes, they bear a higher likelihood of defaulting in this unsettling market situation.

Yet his insight is, of course, fact-based. Not only has the U.S. Federal Reserve decided earlier this month to purchase high-yield bonds into its asset to strongly assure the market, but a long-time cycle analysis into high-yield bonds has shown a pattern of recovery after each major economic crisis.

“Concerns surrounding COVID-19, lower oil prices and a global recession have clearly weighed on markets and while defaults will almost certainly increase going forward, it is worth pointing out that high yield has weathered crises like this before ― and has a history of recovering relatively quickly,” Horne wrote in the email interview.

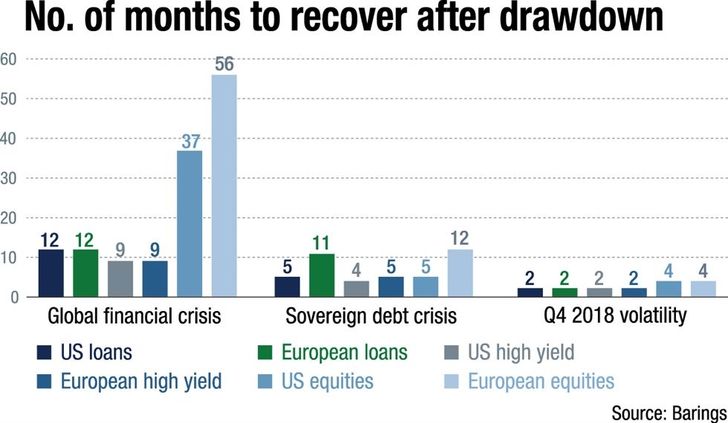

“Lasting anywhere from a few weeks to several months, periods of volatility and disruption in the markets have often been followed by recovery and gains―such as during the global financial crisis (2008), European sovereign debt crisis (2011), commodity crisis (2016) and late 2018 volatility,” he explained, reiterating financial markets' long-term tendency that, almost without exception, periods of recovery and gains follow periods of dips of the market.

“While every crisis is different, we have been in similar situations before ― and we know that ultimately, times of crisis can also yield significant opportunity if navigated carefully,” he stressed.

Fallen angels' increased presence offering quality in high-yield bonds

He also stated that the increase in the number of so-called “fallen angels” ― major companies that have lost their investment-grade (IG) ratings to a high-yield rating ― could also work in investors' favor.

In his latest analysis report, Horne stated citing J.P. Morgan's estimates that about 4 percent of the IG bonds, or as much as $215 billion of debt, could be downgraded to high-yield within this year. Late last month, Ford Motor Co. has also become a fallen angel, as its credit rating was downgraded.

“Fallen angels have been top of mind since they began spiking in mid-March, with market participants understandably worried about the high-yield market's ability to digest this supply without re-pricing the entire market lower,” he said.

“However, it was the U.S market that had the largest potential exposure to fallen angels and now the U.S. Federal Reserve are able to buy these names, the tail risk for the asset class has arguably been reduced materially,” he added, noting that with regard to the companies themselves, these tend to be higher-quality, large corporations with established lines of business and operational flexibility.

“There are a number of higher-quality companies that are trading down significantly despite being largely sound from a fundamental perspective and unlikely to experience a massive disruption to earnings,” Horne emphasized.

Martin Horne, Barings' Head of Global Public Fixed Income & Head of Global High Yield / Courtesy of Barings

Bottom-up credit selection

As a way to manage risks and avoid possible defaults of high-yield bonds, he said fundamentals and bottom-up credit selection are as important as ever.

“At Barings, we aim to select credits that can withstand headwinds and hold up through credit cycles. We also take an active approach to investing, which allows us to move away from credits that exhibit fundamental weakness in favor of healthier issuers,” he said, elaborating that the investment firm's global team ― consisting of more than 70 investment professionals across the U.S. and Europe ― is in constant communication to capitalize on opportunities as well as avoid unwanted risks.

He also warned that there exists varied differences in terms of the vulnerability of each sector. He expected energy and retail could face some of the most challenging times among industries.

“It's not surprising that industries incurring a direct blow from the pandemic have been hardest-hit. Energy, which has been under pressure for the last several years, is a prime example. In addition to the pandemic, the sector is under tremendous pressure from the decline in oil prices, and it's not out of the question that we could see a steep rise in defaults going forward,” he said.

“Retail is another ― comprising many highly levered businesses already facing secular challenges, the industry is now confronting the very real prospect of stores being shut down for weeks or months at a time,” he stated, yet adding that the majority of high yield issuers have the flexibility to continue to service their debt, especially if the period of economic weakness proves to be temporary.

Food manufacturers, cable providers and packaging companies, meanwhile, are the sectors that Horne foretells to be operating rather intact compared to other sectors. He also expected cinema businesses, travel companies and sports franchises to perform on solid footing for the long-term, although these businesses may require short-term liquidity to move through the current pain.

Martin Horne, Barings' Head of Global Public Fixed Income & Head of Global High / Courtesy of Barings

Tips for savvy investors

Lastly, he highlighted the need to have a steadfast focus on companies' fundamentals and bottom-up, credit-by-credit analysis to figure out bond issuers' potentials to thrive long-term, beyond today's events.

“As we look at the markets today, we think there are benefits to a more flexible approach, whereby managers shift allocations between bonds and loans (and across geographies) as prices decouple from fundamentals and relative value emerges,” he said.

“In addition to the opportunities we see in traditional high yield bond markets, opportunities are also beginning to appear in other areas of below investment-grade credit, such as senior secured loans and distressed debt,” he concluded.