Bad loans weigh on banks, card firms

By Lee Kyung-min

An increasing number of small- and medium-sized enterprises and low-income households are failing to make interest payments on time, a sign that these relatively vulnerable groups are beginning to feel the pinch of the economic slowdown.

According to the nation's three major commercial banks ― Shinhan, KEB Hana and KB Kookmin ― and the state-run Industrial Bank of Korea (IBK), the default rate for SME loans has increased over the past few months.

The IBK saw the highest default rate in the first quarter of 0.61 percent in March 2019, up from 0.53 percent at the end of 2018.

KB Kookmin Bank saw the rate jump to 0.31 percent from 0.26 percent in December. A year earlier, the rate was 0.22 percent.

KEB Hana's rate rose to 0.48 percent from 0.41 percent during the same period, while the comparable rate for Shinhan was 0.34 percent, up from 0.29 percent.

Korea Institute of Finance (KIF) researcher who refused to be named said the rising default rate is a byproduct of stricter lending rules for consumer loans.

The Moon Jae-in administration's anti-speculation measures, including stricter consumer lending and heavier taxes, put the banks in a strained position as many of their non-corporate would-be customers are now unable to borrow as much money to buy properties for “investment” for short-term gain.

“Major banks have turned to corporate customers, mostly small businesses and the self-employed, as they were not able to give out loans to households. This in turn has resulted in a balloon effect. The strengthened rules to curb soaring household debt has jacked up risky corporate debt,” he said.

The bigger problem, in his view, is that the current economic slowdown will only hurt their business prospects.

“People are not spending money, and consumer sentiment will keep hitting bottom. This may well raise concerns that more SMEs may be unable to make interest payments on time,” he said.

According to a survey of 500 small businesses by the Korea Federation of SMEs released May 3, one out of three has considered either shutting down or temporarily closing over the past year.

Over 80 percent said business this year has deteriorated compared to last year. Over half, or 53.4 percent said they saw no hope in the economy.

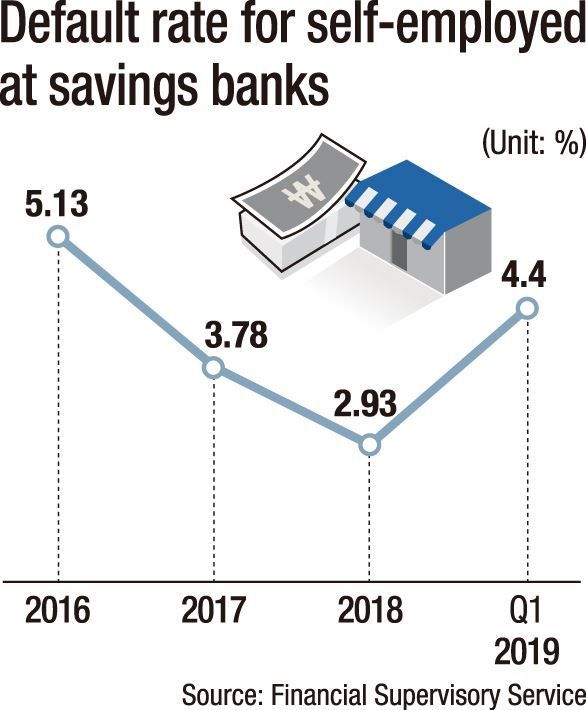

According to the Financial Supervisory Service (FSS), the default rate for the self-employed at savings banks in the first quarter jumped to 4.4 percent from 2.93 percent in December 2018.

The figure was 3.78 percent in 2017 and 5.13 percent in 2016.

The situation is not that different from individual borrowers.

Korea's seven card firms all saw an increase in their default rates in the first three months of the year.

They are Shihan, Samsung, Hyundai, Lotte, Woori KB Kookmin and KEB Hana.

The seven card firms saw their default rate average 1.71 percent, up 0.17 percentage points from the year before.

The relatively riskier loans given out by card firms or auto financing firms are sought mostly by low-income, low-credit people as the screening process for the high interest rate loans is not as stringent as that of the major banks.

Instead, they charge up to a 20 percent annual interest rate, driving economically vulnerable people into bankruptcy faster.

The Credit Finance Association (CFA) said the rise in such numbers is indicative of how people at the lower end of the economic scale are bound to suffer first when the economy begins to falter.

“Low-income households and self-employed people with low credit scores have nowhere else to turn to other than the lenders that charge high interest rates because they need money to live,” a CFA official said.

Yun Chang-hyun, an economist at the University of Seoul, said if those people become unable to find any source of financing, their credit risk could in theory have a spillover effect to industry.

The bigger problem is that the increase in the default rate is a result of the income-led growth policy defined by a near 30 percent increase in the hourly minimum wage over the past two years and reducing the maximum working hours to 52 a week from 68.

“Those who cannot make payments on time are working in minimum wage jobs. They have been struggling as many SMEs have cut the number of workers following the wage hike due to soaring labor costs,” he said.

“The situation requires further monitoring given the economy will be further clouded by low growth, and a decrease in both household and corporate income,” he added.