Wallets slim down as mobile wallets fatten up

Hana SK mobile card user checks the card’s discount benefits on her smartphone in this photo. Hana Financial Group was the first to launch a mobile card in 2010 and, as the No.1 player in the sector, is seeing a steady rise in users. / Courtesy of Hana Financial Group

Mobile card sector grows

but obstacles remain

By Kim Bo-eun

Lee Jae-hyung, a 28-year-old graduate student, has been adding point cards to his smartphone since they were first made available around two years ago. He now has 14 cards stored on his phone.

“Honestly, there are simply too many to carry around in my wallet,” said Lee, who likes to keep his wallet light. “It also saves me the trouble of having to get them reissued if I were to lose my wallet.”

Among the stored cards are his telecommunications company card and others on which he can save points at retail stores, bookstores and movie theaters.

He also mentioned Passbook, an application on Apple’s iPhone, where one can register the numbers of cards that don’t have mobile versions and receive a bar code or QR code that directs points to one’s card.

When asked whether he would be willing to use a mobile card, Lee said he would.

Mobile wallets

Like Lee, an increasing number of smartphone users are getting rid of plastic cards and adding mobile versions to their phones.

In a survey conducted by online and mobile research firm Tillion on 20,000 smartphone users aged 15 and above, 65 percent said they had used smart wallet functions in the past three months.

Of those who used smart wallet functions, 75 percent said telecommunications company SK Telecom’s affiliate SK Planet’s Smart Wallet was the function they had used most frequently in the past month.

Smart Wallet is an app that can store various cards, such as credit cards or membership cards, through which people can save up points. It also enables users to charge their mobile phones with mobile gift vouchers, which can be used at the country’s five main convenience stores, a bookstore chain and movie theater.

The survey indicated that those using mobile wallet functions had an average of 6.4 cards in there, including membership point cards and credit cards.

In response to the growing demands of smartphone users, the banking sector, mobile communication companies and smartphone manufacturers have jumped on the boat to create their own smart wallets.

Telecommunications company SK Telecom has its Smart Wallet, KT its Mocapay and LG Uplus its own Smart Wallet. Finance companies have also been providing their own mobile wallets. Smartphone manufacturers such as Samsung Electronics, Google and Apple offer Samsung Wallet, Google Wallet and Passbook, respectively.

Mobile purchases

Purchases are made by mobile devices such as the smartphone using one of two methods: the cloud method and the near field communication (NFC) method. The method used depends on where the data is stored.

In the cloud method, the credit card information is saved on an online cloud server, which is accessed by wireless communication. Mocapay and British telecommunications, internet and financial services provider O2’s Priority Moments uses the cloud method. All a user needs is a smartphone and the application. This method is applicable to today’s communication and e-commerce environment. However, it is more suitable for online transactions than offline, as the data is stored online.

On the other hand, the NFC method saves the data on the user’s smartphone. American mobile payment system Isis is an example. In order to use the NFC method, users need a chip set that contains NFC functions, and sellers need a mobile chip reader. Most smartphones launched in the nation since last year, with the exception of the iPhone, have NFC functions. However, the readers have yet to become widespread, which is hindering the spread of the NFC method.

Mobile credit cards work by the latter method. A mobile credit card is downloaded on the finance universial subscriber identity module (USIM) chip in the user’s smartphone. In order to be able to use a mobile card, users need to have a smartphone that is registered under their own name.

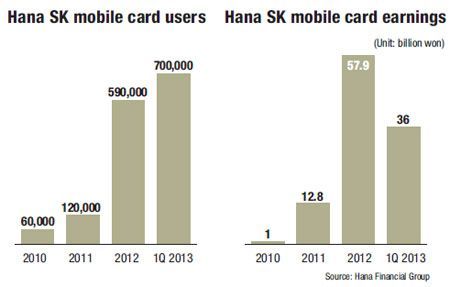

Hana Financial Group became the first to launch a mobile card in 2010, and is now enjoying the indisputable No.1 position in the mobile-card sector. Together with the growth of smartphone users, users of Hana SK card’s mobile version have been rising.

They numbered 60,000 in its first year, which doubled to 120,000 in 2011. The last quarter of 2012 marked 590,000 users and the first quarter of this year 700,000.

Mobile card users are now spending some 360 billion won at discount chains, department stores, coffee shops and online shopping malls.

“We predicted that payment methods would change as smartphones quickly became part of people’s lives. In 2011, there were already 20 million smartphones in use, and the number has risen to exceed 30 million last year,” said a spokesman in charge of the mobile card at Hana.

Fueled by the steady rise in mobile card users, Hana plans to focus more on this sector.

“First, we will try to offer our customers more benefits, such as a 30 percent discount for using mobile telecommunication company cards, a discount unavailable to those using plastic cards,” he said.

He added that Hana will expand its affiliate offline stores where users can pay with their mobile cards. “Up till now we have been concentrating on online payment services, but from now on we will try to focus more on increasing the number of offline stores where mobile cards can be used.”

Currently, users are able to use their mobile cards at the three major discount chains E-mart, Lotte Mart and Home plus, as well as at Hyundai Department Stores and coffee chains such as Starbucks and The Coffee Bean & Tea Leaf.

The spokesman said that Hana is heightening its competitiveness in terms of technical skills. It currently holds a patent for mobile card services and has six others pending.

Obstacles

In time, analysts say, plastic cards will disappear, to be replaced with mobile cards. But it does not look like this will happen anytime soon.

Apart from the fact that many people are comfortable using their plastic credit cards, the infrastructure needed for greater usage of mobile cards does not yet exist.

In fact, only a handful of offline stores, mostly affiliates of conglomerates, currently offer mobile card payment services. This is because the stores need to have mobile touch readers that are able to read the USIM chips. The readers cost around 150,000 to 200,000 won, so mom-and-pop stores have not been eager to buy them.

Lack of infrastructure remains a fundamental obstacle to widespread use of mobile cards. Recently, however, application-based mobile cards that do not need USIM chip readers are being developed. These mobile cards are read through the application by bar-code readers when making payments.

Analysts also point out that currently there is no integrated system that brings the communication firms, finance companies and smartphone manufacturers together.

Kim Jung-wook, managing director of Accenture Korea’s Communications, Media and Technology operating group, said the mobile wallet market, armed with easy payment options for consumers, will promote integration among financial institutions, communication service providers and smartphone manufacturers.

“However, in order to respond quickly to what the market needs, the entire industry, from financial institutions to communication service providers to manufacturers to retailers, needs to work together,” he said.

“We have already witnessed overseas examples in which major retailers collaborate with key stakeholders to develop mobile applications that allow unlimited usage across retail chains,” said Kim. “As expectations for mobile wallets and the payment market grow, there will need to be more collaborative efforts.”