Banks urged to embrace agile transformation - Legacy lenders need to dive deeper

By Choi Jung-kiu

Digital customer journeys are now an essential part of any modern bank's offerings, but despite this clear imperative, six out of 10 financial service companies still fail to achieve their digital transformation goals.

Boston Consulting Group (BCG) works closely with financial institutions across the Asia-Pacific region, offering valuable insights on the importance of putting customers at the heart of transformation goals. In our report, “Taking Digital Banking Beyond Customer Journeys,” we explore the challenges of a truly customer-focused transformation, and the remarkable rewards financial institutions can unlock by delivering on this need.

Our extensive experience supporting financial services partners around the globe tells us that digital transformation must capture the whole customer value stream, from customer-facing, front-end experience, right through to the foundations of process operations, risk, legal and compliance and technology that are ultimately so fundamental to an effective offering. The reality is that creating an encouraging picture above the surface must be accompanied by the right foundations to support sustainable success.

There are two fundamental parts to this journey. First, financial institutions must deeply understand customer pain points and unmet needs. Second, they should deliver the solution not just to customer interfaces, but with a front-to-back, end-to-end perspective that incorporates all relevant functions and roles into one agile team.

Rise of digital banking

BCG's “Global Retail Banking” report revealed that the use of online banking had increased by 23 percent globally, and mobile banking 30 percent over the previous year. This rapid growth has created fertile conditions for ambitious, emerging digital challenger banks, with over 250 of these pioneering banks now operating globally.

Digital transformation now offers an equally powerful opportunity for legacy banks, with our experience revealing successful delivery can reduce costs by 15 percent to 20 percent, improve efficiency and reduce error rates by 20 percentage points to 40 percentage points, and improve customer satisfaction by 20 to 30 points, while delivering a two- to four-fold acceleration in the delivery of new products and services.

Customer journeys are a pivotal part of this transformation. These journeys can come in many forms, but banks' own responsibilities are broadly characterized in five ways ― helping customers open new accounts, helping them borrow money, helping promote financial well-being, helping with transactions and payments and helping solve problems and issues.

This transformation is not without its challenges. We see four common mistakes as banks seek to digitalize: First, investing big in digital focused on customer front-end experience, but neglecting back-end processes. Second, investing in automating the back-end, but failing to fundamentally resolve customer pain points. Third, investing in transforming and modernizing legacy technology, without addressing disconnects between IT and business processes. Fourth, fragmented investment silos that maintain the status quo.

gettyimagesbank

An agile approach to value streams

Banks seeking to remain competitive must embrace agile ways of working, ensuring that speed and flexibility are central to modern operations.

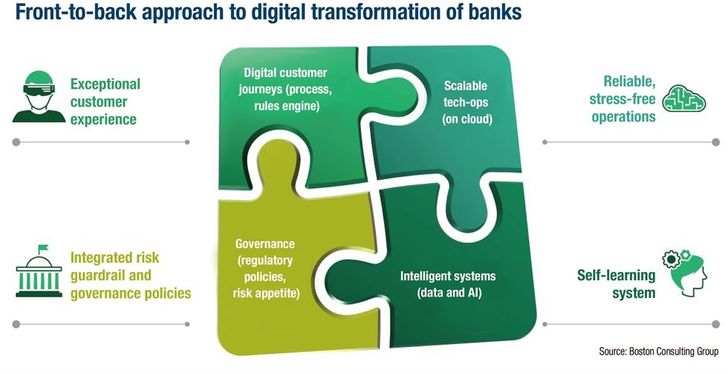

Moving to a front-to-back approach focused on customer value streams is a powerful opportunity to drive forward successful digital transformation. That means enhancing digital customer journeys, scalable tech-ops, governance and intelligence systems.

Customer journey digitalization should leverage world-class interfaces and workflows to deliver tangible and meaningful changes for customers. A focus on enhancing workflow processes from the customer perspective, with human-centric design principles, is critical.

Scalable tech-ops means preparing for growth in a rapidly evolving landscape. Leading institutions often leverage cloud technologies and advanced technology architecture to power these journeys in a scalable way. Unifying security and related functions in a “cyberfusion” approach, alongside robust digital anti-fraud capabilities, is also pivotal. Ultimately, good technology infrastructure is flexible, scalable and reliable.

Intelligent systems should utilize data science to support “smart” processes, with a self-learning system that continuously enhances insights on customers and processes. This will deliver hyper-personalized experiences to each customer. It requires data lake infrastructure that capture this information to generate ongoing insights.

Governance and policy guardrails create the framework to maintain this ecosystem. Customer journey, technology and market intelligence should all channel through a lens of risk and governance policies and procedures. These guardrails are established and then codified into the rule engines, models, workflows, deviations, escalations, flags, access privileges and so on.

Digital transformation is not a static journey ― it's a continuous, ongoing commitment. Holistic customer journeys should be at the heart of this process. An agile approach is vital to delivering on this opportunity, embedding a flexible, adaptive business culture that can respond and react to rapidly evolving market conditions.

The front-to-back approach is a structured process for executing the transformation and digitization of each value stream. Agile teams assigned to design and implement the components of the transformation constitute permanent modifications to the bank's organization and operating model, but one which will evolve over time, as the value stream and focus they look to address also change.

Leading banks are already at the forefront of this customer-focused transformation, creating a new competitive imperative for those left behind. Now is the time for legacy institutions to transform, to test, learn and adapt and realize the opportunity digital delivers for their operations, and their customers.

The writer is a managing director and partner at Boston Consulting Group, Singapore. He has more than 30 years of professional experience across management consulting, international banking, and in leading and growing digital businesses in China and Indonesia. He is a senior fellow at the National University of Singapore, teaching the Digital Transformation Leadership Program to senior executives, and author of the book “The allDigitalFuture Playbook: How to Succeed in Digital Transformation and Innovation in a Complex World.”