Fate of K bank up in the air

K bank CEO Shim Sung-hoon closes his eyes while participating in a National Assembly audit in Seoul, on Oct. 16, 2017. Yonhap

By Lee Min-hyung

The fate of cash-strapped K bank will be determined next week when the National Assembly is set to discuss revising laws on management of internet-only banks here.

Lawmakers plan to bring the issue to the negotiating table on Feb. 26 during a judiciary committee. When the revision is passed, the nation's first internet-only bank will be able to normalize its business by raising capital from its major shareholder, KT.

K bank has suffered from years-long losses since it started in 2017, by failing to increase capital. K bank failed to expand its capital from KT, as regulators disallowed the telecom operator to become the lender's controlling shareholder because of its violation of the Fair Trade Act.

But if a revision is approved, it will allow K bank to receive capital from the telecom company.

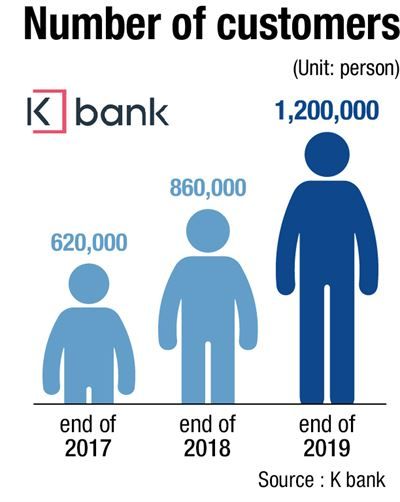

K bank came to the fore with much fanfare in April 2017 as the nation's first internet-only bank, followed shortly after by KakaoBank. As of the end of that year, the number of K bank users reached 620,000. Riding on the online bank boom, the firm expanded its foothold by increasing the number of users to 860,000 by the end of 2018 and 1.2 million by the end of 2019.

Starting from 2019, however, capital-related setbacks meant K bank offered limited services with the firm suspending its loan businesses to customers.

Initially, K bank was supposed to receive 590 billion won ($490 million) in capital from KT to expand its capital to over 1 trillion won. But the Financial Services Commission (FSC) blocked the move, citing KT's violation of the anti-trust law.

With the KT subsidiary facing growing uncertainties about its sustainable growth, Kakao Bank solidified its leadership as the nation's top internet-only bank. Kakao Bank is set to finish its initial public offering this year.

“If lawmakers do not approve the revision, K bank will have to find another major shareholder which has not been mired in the anti-trust-related issue,” an industry official said on condition of anonymity.

“But the best-case scenario is that KT maintains the status as the position and offers the capital to normalize K bank's business,” the official said.

Chances are KT will pass the position onto another subsidiary to bring K bank to a turnaround, according to him.

K bank declined to comment further over the controversy, citing the sensitivity of the issue.

At the end of last year, the outstanding balance of the bank's loans stood at 1.42 trillion won.

Its Bank for International Settlement (BIS) capital adequacy ratio stood at 11.85 percent at the end of September, the lowest level among local lenders. The average ratio among local lenders came in at 15.4 percent.

When the ratio falls below 8 percent, the FSC can interfere in the bank's management to fix its financial soundness.