Kakao Bank on track, while K bank falters

By Lee Kyung-min

Korea's two internet-only banks have shown drastically contrasting earnings results in the third quarter.

Kakao Bank continued to enjoy solid earnings, while K bank suffered from ballooning losses due to a lack of capital curbing its lending business.

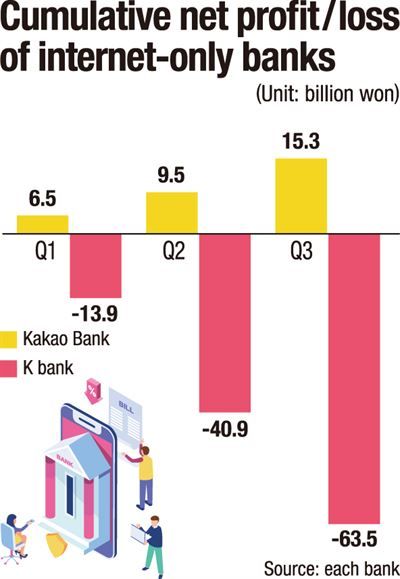

According to data from Financial Supervisory Service (FSS), Kakao Bank reported 15.3 billion won ($13.1 million) in net profit for the first nine months of 2019.

The bank swung into the black in the first quarter for the first time recording 6.5 billion won, only 20 months after it was launched.

Net profit in the first six months jumped to 9.5 billion won thanks to the second-quarter net profit of 3 billion won. This was further boosted by a third-quarter net profit of 5.7 billion won.

In September, Kakao had over 10.69 million customers with a deposit total standing at 19.9 trillion won and lending at 13.6 trillion won.

“Kakao Bank plans to raise 50 billion won through rights offering within November, laying the groundwork for it to become a comprehensive financial service provider,” it said.

In contrast, K bank, the nation's first internet bank, has been suffering from ballooning losses.

K bank reported a net loss of 63.5 billion won in the first nine months of 2019. It recorded a net loss of 22.6 billion won in the third quarter only. Its net losses stood at 13.9 billion won in the first quarter and 27 billion in the second quarter.

The poor performance came as KT, K bank's second-largest shareholder with a 10 percent stake, failed to raise its stake in the lender to 34 percent by participating in its recapitalization after the mobile carrier was investigated over a possible antitrust law violation.

Under a related act regarding internet-only banks, major shareholders should not be guilty of violating financial laws, including antitrust and tax laws, within the previous five years.

Kiwoom Securities senior analyst Seo Young-soo said Kakao Bank has reached what the market considers an “economy of scale,” a certain point beyond which its online-based business model becomes strong and established enough to compete with traditional financial service providers.

“It is all about the economy of scale,” Seo said. “Online-based enterprises are bound to record a net loss for a period of time until their capital and the number of customers become large enough. Now that Kakao has passed that point, its business prospect is much brighter. K bank has yet to and it will need more time.”