Asset management in low-interest era

Saving holds key

.jpg)

A model of vault brand Lucell

By Kim Bo-eun

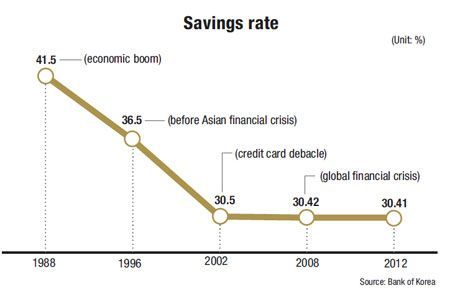

The prolonged economic slump has brought down bank interest rates and savings rates have been declining according

ly. The savings rate stood at 34.1 percent in 2012, the lowest since 1982. Real estate transactions have fallen together with the drop in property prices. Last year, the housing transactions marked the lowest point since 2006.

In an era of low growth, low interest and the sluggish property market, it seems there is nowhere for investors to put money into.

Analysts say playing it safe is the easiest way to make money during hard times. Suggestions include making extra money through savings products that help reduce tax payments. The latest interest-income tax-free savings products have become a must-have for low-income salaried workers and the self-employed.

Savings products with tax benefits

The latest savings product has made a comeback since it was abolished in 1995 due to the shortage in government budget, as it exempts the 14-percent interest income tax.

The measure comes as the government eliminated the tax exemption benefits of the long-term house-purchasing savings through revisions to the tax law last year. It is also part of the government's efforts to encourage savings.

The savings product is restricted to the middle-and lower-income bracket; employees who make up to 50 million won a year or self-employed people who make up to 35 million won.

The savings period is seven years, but it can be extended once for up to three years.

One can save up to 3 million won a quarter, which is a maximum of 12 million a year.

Along with a large tax exemption, the other attractive aspect of the product is the relatively high interest rate, which ranges from 3.4 to 4.3 percent, depending on the financial institutions.

Banks are offering higher rates for customers who make use of additional services, such as applying for credit cards of having their salaries directly deposited to that particular bank. Among them, the Industrial Bank of Korea has the highest rate at 4.6 percent.

The 4 percent plus alpha percent interest rate, however, is only fixed for the first three years. The rate thereafter is subject to change according to the market.

Securities firms are also offering domestic bond and foreign stock options that provide the same tax exemptions. Experts advise dividing one's assets in both savings account as well as in investment funds, as they are long-term products.

“Set a certain amount as your goal, compare the characteristics of each of the products offered at financial institutions and diversify the amoung you save,” Kim Sung-tae, a senior manager at the investment product department at Shinhan Investment Corp., told The Korea Times. “This is a good strategy in terms of stability and profitability.”

Storing wealth in vaults

Starting this year, the standard amount for aggregate taxation on financial income has been lowered from 40 million to 20 million won, which means that those who earn large sums through interest and dividend payments are subject to more taxes.

While tax-free investment options are drawing the attention of large asset owners, others are choosing to store their assets in cash and other items.

Some say that in a low growth, low interest economy, buying gold is the safest method of investment.

In order to stock cash and other items, asset holders are turning to vaults.

According to a spokesperson for Hyundai Department Store, three of its branches, each located in affluent districts in the capital _ in Apgujeong-dong, Mok-dong and at the Korea World Trade Center _ have stores selling vaults. According to him, the department store is planning to open another vault store at its branch in the southeastern industrial city of Ulsan.

“We have been seeing steady sales of vaults, and that is why we've decided to open another store at a branch outside of Seoul,” he said.

The spokesman said that this year, some 50 vaults were sold altogether at the three branches as of March. 7.

Save, save and save

But regardless of whether people fall in the lower-income bracket or own huge assets, saving is key to managing what they have.

According to Park Chang-mo, author of “Secrets of Investment,” it is more effective to increase the amount seaved, rather than to make big money through investments.

Park said low-interest rates are not a temporary phenomenon, but a problem rooted in the overall structure of the economy. He advised that people understand this, and make an effort to save more instead of looking for higher interest rates.

“It is easier and more realistic to collect a larger sum of money by saving 100,000 won more every month, rather than investing 10 million won to make a 12 percent earnings rate,” he told The Korea Times.